and How Carmakers, OEMs, and Tier 1 Providers Should Respond Now

The traditional cockpit has evolved into a digital product similar to smart devices. As part of this evolution, automotive industry actors are encouraged to transform their approach to R&D and the emerging technology to stay relevant.

We expect to see full-scale digitization in the automotive manufacturing cycle by 2030, driven mainly by four mutually reinforcing trends: connected, autonomous, shared and electric (CASE) vehicles. The original equipment manufacturing (OEM) businesses get a new opportunity to generate continuous revenue while meeting the digital needs of their future customers.

Connected, electric and autonomous vehicles are seen as a key technology trend that will affect car cockpits on a large scale. The trend towards car connectivity is driving the rise of two key product categories – the cockpit dashboard (instrument cluster) and the infotainment system, which make up about two-thirds of the digital cockpit.

Just as technology has changed the way people communicate, access food and work remotely, the digital cockpit is changing the way we perceive cars. Vehicles of the future will play a pivotal role in moving towards a smarter and more personalized in-car experience that is software and service-oriented, networked and interoperable.

Technologies such as 5G, edge computing, cloud computing and artificial intelligence (AI) have already begun to influence the automotive industry – the ideal digital cockpit can combine these complex technologies into one access point that is simple and seamless.

The automotive digital cockpit market is segmented by equipment, vehicle type, electric vehicle type and application. Growth between segments helps analyze niche growth areas and go-to-market strategies, as well as identify main differentiators in target markets.

Let’s take a closer look at the size of different digital cockpit market categories.

In 2022, the global In-Vehicle Infotainment market was estimated at $20.96 billion. According to projections, it will increase at a compound annual growth rate (CAGR) of 10.3% during the forecast period (2023-2031) and is anticipated to reach $50.64 billion by 2031. The North American region is the market’s largest contributor and is predicted to grow at a CAGR of 9.9% during the forecast period.

The global Instrument Cluster Market Size is projected to reach $13,610 million by 2026, up from $10,320 million in 2020, at a CAGR of 4.7%.

The head-up display segment is expected to record the highest CAGR of over 15% from 2021 to 2028 thanks to the integration of augmented reality (AR) to improve safety and driving experience.

In 2022, the TFT-LCD display panel market achieved a value of $148.3 billion on a global scale. During the forecast period of 2023-2028, it is predicted to expand at a CAGR of 4.9% and is projected to attain a value of $197.6 billion by 2028.

According to Data Bridge Market Research, in 2021, the global market for passenger vehicles was assessed at $445.00 billion, and it is projected to reach $2641.10 billion by 2029, with a compound annual growth rate (CAGR) of 7.83% during 2022-2029. The use of electric vehicles is predicted to increase significantly in the application segment due to heightened environmental concerns.

Different technologies and components are emerging on the market for digital integrated cockpit systems. Some of these are as follows:

HUD was first used by fighters and is now used in the automotive industry. The HUD is a transparent display that shows information such as vehicle speed, navigation data, obstacle data and more, right into the driver’s field of vision without distraction.

Three types of technologies are used here: C-HUD, W-HUD and Augmented Reality-HUD. HUDs are mainly used for luxury vehicles, but as customer needs grow, Tier 1 suppliers are planning to implement HUDs on commercial and passenger cars, as well. The future of HUDs are 3D HUDs, voice-controlled HUDs and laser HUDs.

The digital instrument cluster provides the driver with a variety of information that dynamically adapts to the current driving situation. The digital cluster is ideal for a wide range of possible application scenarios, including conventional tacho displays, function displays, route planning charts or displaying video from a rear view camera.

It allows the drivers to keep tabs on the car performance indicators in real-time. This provides fewer to zero distractions and helps reduce the risk of an accident. The information is very easy to read in all situations, thanks to the outstanding display resolution. Thanks to its capabilities, the human-machine interface (HMI) can be personalized and easily adapted to different vehicle models and markets.

The infotainment system, as the word suggests, is a combination of information and entertainment. Basically, an infotainment system is a set of hardware and software in vehicles that provide audio and video entertainment/information. Infotainment systems play an important role in making the driving journey enjoyable and safe.

As the automotive tech industry continues to grow, older infotainment systems are being replaced by advanced systems with high definition screens and improved connectivity such as WiFi, Bluetooth and USB. HD touchscreens are built into the car’s dashboard for the driver to access or in the rear seats where passengers can use them. It can be operated using the touch screen or with remote controls.

A car navigation system uses navigation satellites to determine the location of a specific place or person (via a mobile phone). These systems are not limited to indicating the location of a place or person. They also provide information on nearby hotels, restaurants, hospitals, gas stations, traffic congestion, shortest route and other similar information, which is analyzed and optimized using various ML algorithms.

Nowadays, every vehicle comes pre-installed with heating, ventilation and air conditioning. The HVAC system is used to monitor the temperature inside the vehicle. Previously, knobs were used to regulate the temperature, but as technology evolved, they were replaced by automatic temperature controllers consisting of thermal sensors installed inside the car. Thermal sensors detect the temperature outside the car and send the data to a programmable controller, which then adjusts the temperature inside the car (according to an algorithm).

From managing audio/video information to controlling multiple vehicle functions, the intelligent voice assistants enable drivers and passengers to perform multiple tasks hands-free.

According to Business Insider, in the United States, in-car voice assistance is more popular than smartphone assistance thanks to the hands-free experience it provides. Modern connected vehicles are developed with built-in voice assist systems that take the driving experience to a whole new level.

As per Voicebot.ai, there’re currently 127.1 million consumers of voice assistants in the USA alone – that’s an impressive audience.

Tech giants like Apple and Google have developed extensions/apps for connected car operating systems that can be linked to the dashboard display via USB or Bluetooth / WiFi. Such solutions include Apple CarPlay and Google Android Auto – two apps specifically designed to control connected vehicle systems. More than 70 car manufacturers use Android Auto, and more than 50 car manufacturers use CarPlay as their smart voice assistant, according to Business Insider.

In-vehicle applications – braking, ABS, self-parking, and more – are being developed within complex digital cockpits. And just like a computer or mobile phone, these apps are built on standard operating systems; this is called a middleware product. Middleware allows developers to focus on their innovations through their applications.

Middleware provides basic functionality such as communications, memory management, scheduling, and I/O. It removes the development overhead associated with taking care of these details, allowing you to focus entirely on the specific purpose of your application.

Today’s automotive middleware is based on two standardized platforms:

Creating unique and sustainable driving experiences and consistently engaging consumers throughout the vehicle-ownership life cycle presents a complex challenge for automotive companies. The fact that consumers’ interaction with brands has changed drastically in the past years exacerbates that challenge.

The following factors could push car companies to create innovative business models that will change the way OEMs and dealers interact with their customers:

As customer demands for connected cars become more sophisticated, new challenges emerge for car makers and OEMs.

As an example, drivers expect the car to be ready to go as soon as they get inside or turn the key. This is very different from other areas that use software platforms.

Imagine walking to your car in a parking lot with many other cars. As you get closer, your car detects you approaching and starts booting the system, while keeping the display dark. When you’re seated and ready to start the car, the display lights up, presenting you with an immediately up-and-running system.

Moving forward, brand identity alone will not suffice to maintain the level of customer loyalty that automakers currently have. As more connected features become available, consumers will pay more attention to the features than the brand logo. They now want to integrate features into the car that enhance the driving experience within their connected driving cycle. IoT capabilities such as lane departure detection and over-the-air (OTA) software updates will influence shopper decisions.

To maintain customer loyalty, automotive brands must also successfully integrate connected customer lifestyles through digital services. This will allow consumers to interact with their cars in the same way they use their own familiar connected devices such as smartphones. Realizing that sales will be influenced by services and features rather than brand reputation, automotive companies will need to provide the same hassle-free and intuitive in-vehicle experience as using a smartphone. According to Ericsson, this is especially relevant since services are expected to account for 54% of the global revenue from connected cars by 2025.

OEMs and Tier 1 providers are well positioned to monetize their direct access to customers and data, as very few companies have such regular and extensive interactions with their end consumers.

Despite the potential, many automotive companies have only scratched the surface of data monetization, and their efforts often fail because they create inconvenience for customers and run into performance issues, resulting in low retention.

For example, many of them have complex registration and login processes on different devices or complex interfaces, which puts OEMs at a disadvantage compared to companies that offer the relative simplicity of one-click smartphone solutions.

The approach that emerging electric vehicle (EV) makers are taking to tackle this problem is different from that of traditional companies. They use customer feedback and continually improve their products based on information.

EV OEMs also have very short reaction times and are ready to release beta versions, which they later improve with OTA updates. For example, one OEM hired rinf.tech to develop and release a feature to correct vehicle warnings within six weeks in response to their customer request.

In parallel, consumer technology market players are also leveraging their in-house expertise to develop operating systems (OS) that provide access to a complete ecosystem of internal and external digital cockpit applications such as cards. Again, their approach is more similar to that of smartphones than cars.

Some OEMs and suppliers are gradually waking up to this new world and developing better infotainment solutions and applications. Others are taking a different path and integrating complete infotainment solutions developed by tech players, with some already announcing these projects. However, OEMs and suppliers still have a long way to go to fully focus on the customer.

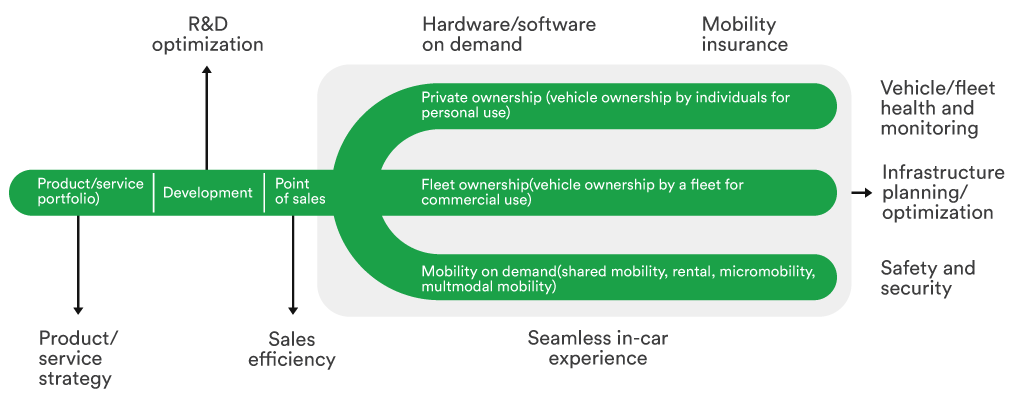

To drive connected car data monetisation and improve CX, OEMs and Tier 1 providers should focus on the following 9 clusters, as per McKinsey:

These nine clusters could generate $250 billion to $ 00 billion in annual added value for players across the connected car ecosystem in 2030.

It’s important to consider software product stickiness principles when developing digital cockpit and other automotive technology solutions.

Product stickiness is a feedback loop that measures user value and, more broadly, business value. Not only are sticky products a pleasure to use from time to time, they become part of our daily life, and that could be the secret to customer retention for automotive companies.

Stickiness is a common goal that connected car programs should strive to achieve. The degree of user improvement in a product depends on the ease of use and the uniqueness of the feature set. The stickiness aspect is important for connected car products in general and digital cockpit in particular because the competition goes beyond the automotive industry.

In a connected car world, a competitor is simply a third-party mobile application that can reduce the need for customers to use the embedded features provided by automotive OEMs.

To enable digital cockpit stickiness, it’s highly recommended to build solutions around the 5E concept:

Differentiated customer experiences can be influenced by design, quality, and time of gaining that experience.

Now let’s delve into details of how personalization, AI and voice technology, IoT, and security help build new customer experiences and gain a competitive edge.

The car infotainment system has evolved from radio, cassettes and CDs to car navigation systems, video players, USB and Bluetooth connectivity, car computers, in-car internet and WiFi.

In addition to this, the widespread availability of entertainment content and the need for information related to driving are factors fueling the demand for multifunctional infotainment systems.

Consumers are increasingly demanding more advanced and personalized infotainment features.

In addition to basic infotainment and personalization features, drivers are showing a strong interest in the following features, according toDeloitte’s 2019 Automotive Consumer Survey:

Tier 1 providers need to consider designing and integrating infotainment systems and applications, including interfaces to home devices and links to offices. In addition, OEMs can sell advertisements during autonomous shared travel, just as public transportation does today.

The in-car infotainment system finds application in infotainment, navigation, communication and network services, remote services and telematic services with over-the-air (OTA) updates. In developed markets, people also use infotainment systems to access social media and email, check city parking spaces, and stream HD audio and video.

Advanced infotainment features combine both user behavior and next-level data-driven infotainment systems. They can add power to the on-board IVI system by manually personalizing the media playlist or automating entertainment selections based on user behavior data.

Driver behavior data is derived from analytics using interactive voice recognition based on the mood of the vehicle owner.

The architecture should provide intelligent profiling with both interactive voice recognition systems and pattern recognition algorithms without compromising client privacy.

Important considerations for building advanced IVI systems:

The growing smart home market and the need to connect drivers to their external environment force car manufacturers to rethink their development strategies and partnerships. Connecting to broader intelligent infrastructure will require integrating a range of partnerships and platforms into the vehicle.

Interconnected devices such as smartphones and smart cars have changed our way of life and made it more convenient. Consumers are always looking for custom solutions and smooth transitions out of the car.

Aspects related to interoperability, user interface and implementation are important areas for proper solution design.

Important considerations for building automotive IoT solutions:

According to Deloitte, 62% of German and 59% of American car buyers are extremely concerned about data security.

Fifty-nine per cent are aware that data can be collected from their vehicles.

While 83% of consumers are aware of the European General Data Protection Regulation (GDPR), 40% of them believe it impacts data protection.

While consumers are concerned about their digital cockpit security and data safety, only 10% of car makers have an established cybersecurity team, as per a recent Ponemon Institute study. As vehicle functionality becomes more software-based, manufacturers will need to prioritize more reliable testing and safety measures investments.

Original equipment manufacturers continue to focus on consumer privacy and safety as software vulnerabilities can undermine the security of connected automotive systems and functions, compromising user privacy and physical security. A single accident can destroy a brand’s reputation, making it very difficult for consumers to return.

With this in mind, we at rinf.tech provide secure connection management and isolate the Internet of Things from other cellular traffic by encrypting it. In addition, we use abnormal activity alerts and robust identity and access management to maintain the IoT network security.

The bulk of the responsibility to deliver highly secure and compliant digital cockpit solutions rests with OEMs. They should consider the ecosystem as a whole and develop strategies to protect the components under their direct control and educate and inform end users about the protection of the components they control. While not only their responsibility, OEMs stand to benefit if they are aware of the security and privacy aspects that customers need to be aware of.

It will benefit customers and bring OEMs into the spotlight if they make efforts to raise awareness of the following factors:

From an enterprise perspective, OEMs need to secure their digital cockpit solutions and include aspects such as authentication and authorization between the two components, session establishment and maintenance. Some other security aspects that Tier 1 manufacturers need to build into their solutions include the following:

Regulations will play a vital role in the implementation of connected, highly automated vehicles. Governments and regulators are now working with automakers to improve transportation by addressing key issues such as traffic congestion, accidents and costs. As part of this effort, governments would like to introduce features such as automatic braking and lane-departure warnings that have been shown to reduce accidents.

While these capabilities are primarily based on in-vehicle services, connectivity can help extend the driver’s line of sight beyond the immediate range of onboard sensors. As a result of these new technologies, the Advanced Driver Assistance Systems (ADAS) segment is expected to grow to$ 36 billion by 2025, with a CAGR of 30.8%, according to Statista.

The need for limitless coverage poses another challenge for digital cockpit. Local data and sovereignty rules complicate connection management by affecting where the collected data can be analyzed and stored when a vehicle crosses borders to different countries or regions. Inconsistent guidelines will have a negative impact on adoption and usage. However, if the EU regulatory framework proves to be effective, 43% of vehicles could be partially or fully autonomous by 2035.

Today’s connected car capabilities provide a differentiated value proposition. It is expected to become a commodity in the future. The key to maximizing its potential is to continuously innovate and improve customer service over time. Key considerations for any automotive player along the way include the following:

We provide a robust infrastructure, scalable, data-centric architectures and both mainstream and new tech stacks for successful digital cockpit solutions development and testing.

Some of the world’s leading automotive brands and Tier 1 providers have been trusting us the development of their custom digital instrument clusters, infotainment, and middleware solutions since the advent of the connected car.

Contact us for client references!

We have our own R&D Embedded and 4 Delivery Centers in Romania (Bucharest and Timisoara), Ukraine (Kyiv), and Sofia (Bulgaria). This allows us to have access to the pool of around 400K software engineers, testers, IoT developers, AI developers, data scientists, cybersecurity and other tech specialists with different skillsets.

Using our R&D teams and proven methodologies, we can deliver a PoC project within a very short timeframe.

Rinf.tech has a representative office in Detroit, MI – the center of the American automotive industry and innovation labs and R&D.

Our dedicated multifunctional teams are fully Agile and ready to operate in synergy with your in-house teams to support your product development across all stages, from design to release. We provide deep technology consulting throughout the entire lifecycle of your automotive solution.

Copyright © 2023 rinf.tech. All Rights Reserved.

Terms & Conditions. Cookie Policy. Privacy Policy.

Politica Avertizari de Integritate (RO)